The business can interpret how the sales figures are affecting the overall profits. On the other hand, variable costs are costs that depend on the amount of goods and services a business produces. The more it produces in a given month, the more raw materials variable cost definition it requires. Likewise, a cafe owner needs things like coffee and pastries to sell to visitors. The more customers she serves, the more food and beverages she must buy. These costs would be included when calculating the contribution margin.

Example: contribution margin and target profit

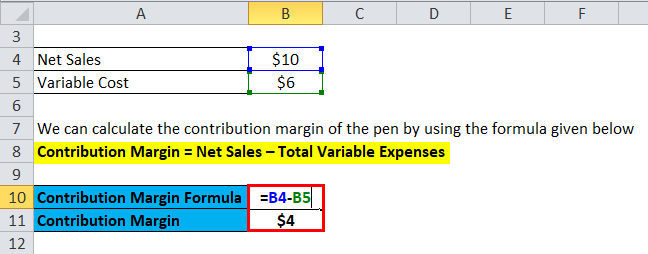

Now, let’s try to understand the contribution margin per unit with the help of an example. Variable Costs depend on the amount of production that your business generates. Accordingly, these costs increase with the increase in the level of your production and vice-versa. This means the higher the contribution, the more is the increase in profit or reduction of loss. In other words, your contribution margin increases with the sale of each of your products.

Contribution Margin Ratio

These costs may be higher because technology is often more expensive when it is new than it will be in the future, when it is easier and more cost effective to produce and also more accessible. The same will likely happen over time with the cost of creating and using driverless transportation. The contribution margin ratio refers to the difference between your sales and variable expenses expressed as a percentage. That is, this ratio calculates the percentage of the contribution margin compared to your company’s net sales. Fixed costs are the costs that do not change with the change in the level of output. In other words, fixed costs are not dependent on your business’s productivity.

Contribution Margin: What Is It and How To Calculate It

- It provides one way to show the profit potential of a particular product offered by a company and shows the portion of sales that helps to cover the company’s fixed costs.

- Variable expenses directly depend upon the quantity of products produced by your company.

- If all variable and fixed costs are covered by the selling price, the breakeven point is reached, and any remaining amount is profit.

- However, if there are many products with a variety of different contribution margins, this analysis can be quite difficult to perform.

It is important for you to understand the concept of contribution margin. This is because the contribution margin ratio indicates the extent to which your business can cover its fixed costs. The contribution margin measures how efficiently a company can produce products and maintain low levels of variable costs.

To get the ratio, all you need to do is divide the contribution margin by the total revenue. Thus, the concept of contribution margin is used to determine the minimum price at which you should sell your goods or services to cover its costs. Therefore, it is not advised to continue selling your product if your contribution margin ratio is too low or negative. This is because it would be quite challenging for your business to earn profits over the long-term. The contribution margin ratio is also known as the profit volume ratio.

Variable Costs

Break even point (BEP) refers to the activity level at which total revenue equals total cost. Contribution margin is the variable expenses plus some part of fixed costs which is covered. Thus, CM is the variable expense plus profit which will incur if any activity takes place over and above BEP. Typically, variable costs are only comprised of direct materials, any supplies that would not be consumed if the products were not manufactured, commissions, and piece rate wages.

It is considered a managerial ratio because companies rarely report margins to the public. Instead, management uses this calculation to help improve internal procedures in the production process. It means there’s more money for covering fixed costs and contributing to profit.

A high contribution margin indicates that a company tends to bring in more money than it spends. The analysis of the contribution margin facilitates a more in-depth, granular understanding of a company’s unit economics (and cost structure). Further, it is impossible for you to determine the number of units that you must sell to cover all your costs or generate profit.

Profit is any money left over after all variable and fixed costs have been settled. You can calculate the contribution margin by subtracting the direct variable costs from the sales revenue. If all variable and fixed costs are covered by the selling price, the breakeven point is reached, and any remaining amount is profit.